How Reliable is Social Security?

Americans love making light of the government. Whether that’s joking about the IRS or slow mail delivery from the Post Office. Social Security is also an easy punching bag, “No way I’m going to get my Social Security the way things are going!” is a common jab. But sitting behind joking statements like this lies a real life, unspoken question – “Should I count on Social Security in Retirement?”

What Does Social Security Do?

The Social Security Act was passed in 1935 during the presidency of Franklin Roosevelt. America was five years into the Great Depression and on the cusp of entering World War II. The purpose behind it was to provide a monetary safety net for those unable to work as a result of age or a disability. The one big difference between then and now is that life expectancies have increased by 20 years. If you turned 65 in 1935, they didn’t expect you to live much longer. Now, people regularly live into their 80s and 90s, making the program as much a retirement benefit as an income safety net in old age.

Who Benefits Most?

Americans at lower income levels receive more income replacement benefits relative to what high earners get.

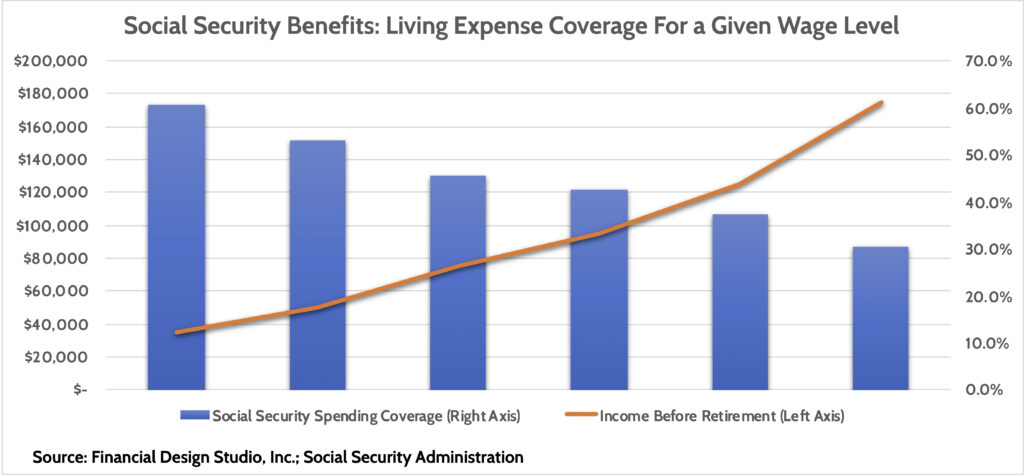

We’ve created a chart showing potential Social Security benefits for a new retiree at various income levels, all else equal.

For example, on the left side of the chart we have someone who currently earns $35,000 per year and will retire soon. After taxes, their take-home pay is $24,500. We’ll assume this is the money they live on; their living expenses.

This person would receive $1,241 per month in benefits, which comes out to $14,892 per year.

If we compare that benefit to what they normally spend, we find that Social Security will cover just over 60% of their living expenses while in retirement.

Notice what happens as income levels increase. Someone making $75,000 per year will receive less than 50% coverage of their living expenses. All the way to the right we see that the percentage drops to 30% coverage for the $175,000/year earner.

Will Social Security Benefits Keep Up With Inflation?

We’ve seen how important Social Security income can be for your retirement spending needs. Yet we all know that living expense costs go up each year because of inflation.

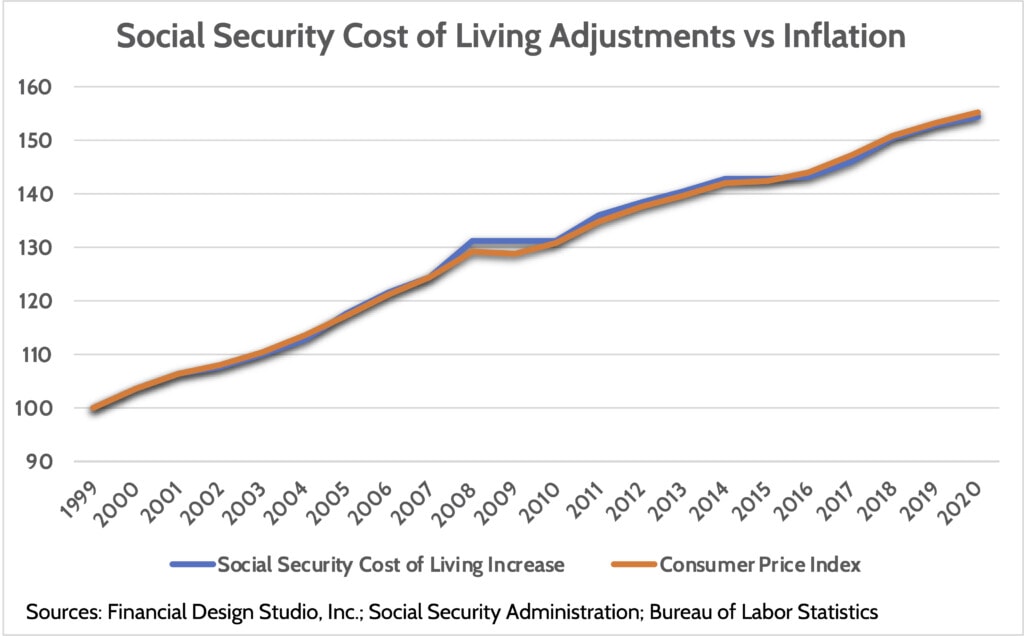

Most company pensions and insurance annuities will ‘guarantee’ a flat monthly payment for as long as you live. The prohram takes this feature one step further by giving you a cost-of-living adjustment each year. These adjustments – often called a “COLA” – maintain the real purchasing power of your income.

Officially, COLA adjustments have been doing their job. Since 1999, total COLAs have almost perfectly matched the officially reported inflation rate.

Can I Count on Getting Social Security in Retirement?

The Social Security Trustees come out with an annual report detailing the financial health of the SS system. And every year, news sites are filled with headlines about how the program will go bankrupt in XYZ year.

Since its inception, Social Security has taken in more payroll taxes than they paid out in benefits. They put these extra dollars into a “trust” to make the accounting work. Think of the trust as a savings account.

Recently, the level of paid Social Security benefits exceeded the amount of payroll taxes coming in the door. To keep everyone’s benefits stable, the Social Security Administration (SSA) has to dip into the pot of money set aside in the trust. By 2034, the SSA expects the trust fund to be fully depleted.

Let me be clear: it will NOT go bankrupt in the sense that the news wants us to believe. It will not go to zero. If the Trust fund is depleted, they would cut benefits to the level of taxes coming in the door.

The worst-case scenario for Social Security is that the trust fund is depleted and Congress does nothing to fix it. In that case, monthly benefits would fall about 20-25%. A retiree getting a $1,000 monthly check would get a $790 check instead.

Building Your Retirement Income Plan Around Social Security

As you think about retirement, start with Social Security. You can go to this website and get your benefits statement online. This will give you your expected monthly benefit in today’s dollars.

Compare that figure to the amount you normally spend each month. The gap between what you’re spending and what SS would provide is what you need to save for.

While your income will stop on the day you retire, your living expenses won’t. That’s why it’s important to have a plan in place to replace that lost income.

If you’re wondering how your retirement income plan might look, please reach out to us. We’ll ask for a Social Security statement and go from there!

As fiduciaries, we’ve taken an oath to prioritize your financial well-being above all else. We’ll treat you with the honesty and integrity you’d expect from someone with whom you are entrusting your future

Joseph Vecchio, CPA, CFP®, MBA, the founder of Shore Financial Planning, started his investment career in 1998 as a professional trader/money manager on wall street. He believes in a passive investing style founded on academic evidence.

Joe takes pride in protecting people from financial predators and helping them make smart financial decisions. We will provide you peace of mind through conflict-free, value-added financial, and tax advice.