Portfolio Rebalancing: What is it and What Are its Benefits

Market fluctuations and the types of investments you have can cause your portfolio to get out of balance. How you react to this can either keep your portfolio in line with your long term goals…or add unnecessary risk to your future. Market ups and downs make it difficult to know when to make adjustments…and when to leave everything alone. But creating a systematic rebalancing plan can help.

WHAT IS REBALANCING PORTFOLIO?

Knowing which stocks buy and sell is difficult for any investor, regardless of their experience.

Asset allocation can make this process much easier.

Proper asset allocation will vary according to each investor’s unique situation and needs. Their portfolio allocation will generally be some combination of stocks, bonds, and cash.

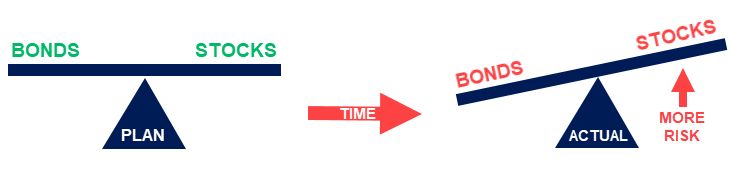

Over time, the relative values of your individual investments will fluctuate. Rebalancing your portfolio is the process of bringing its asset allocation back to your target percentages.

The need to rebalance arises from the uneven performance of different types of investments given varying market and economic conditions.

Rebalancing Your Portfolio: An Example

Let’s say an investor has a simple portfolio with a target asset allocation of:

- Stock ETF allocation: 60%

- Bond ETF allocation: 40%

Over time, the allocation will fluctuate based on market and economic factors.

For example, if the stock market skyrockets and you don’t make any portfolio changes, your allocation might end up looking like this:

- Stock ETF allocation: 80%

- Bond ETF allocation: 20%

At this point, the over-allocation to stocks is causing your portfolio to take on more risk that you might be comfortable with.

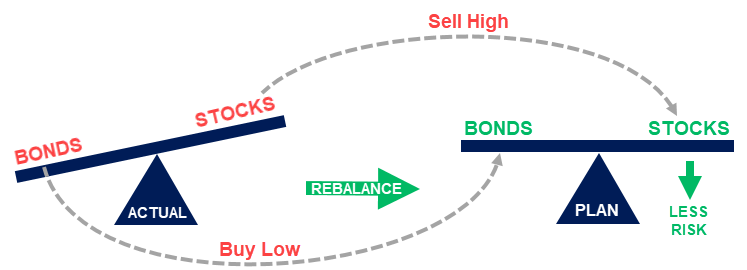

To counteract this, you will want to reduce your exposure to the stock ETF to bring it back down to its target of 60%. This will increase your exposure to the bond ETF and bring its allocation back to its target of 40%.

When To Rebalance Your Portfolio

You should rebalance your portfolio at predetermined intervals, either quarterly, semiannually, or annually. An exception to this would be after a major market move up or down.

Portfolio rebalancing is often accomplished by selling holdings in asset classes where the portfolio is overallocated. Then you redirect those funds to positions in underweighted asset classes.

Another way you can accomplish rebalancing is by adding new money to your portfolio. These new funds should be directed towards positions in underweighted asset classes.

THE TOP 4 BENEFITS OF PORTFOLIO REBALANCING

1) Maintaining Your Desired Risk Exposure and Asset Allocation

The purpose of rebalancing is not to beat the market, it is to manage risk.

While it may be tempting to “let your winners ride” when the market has experienced a period of solid gains, a continued overallocation to stocks can result in outsized losses when the market heads down during the next correction.

2) Buying Low And Selling High

Rebalancing inherently directs investors to sell assets that have experienced higher returns and buy more of the assets that have experienced lower returns.

3) Sticking To A Rules-Based Approach

Money is an inherently emotional topic. These emotions can be further exacerbated by the fact it is impossible to consistently time the market.

This can incite regret at missing that hot stock or new opportunity. Fear of missing out can be a powerful and potentially damaging emotional response.

It’s important to keep your focus on track with your long-term investment plan, and away from the latest headlines. It is best practice to rebalance your portfolio based on predetermined rules.

4) Hold Your Financial Advisor Accountable

Investors place a lot of trust in their financial advisors. Having an IPS in place ensures your advisor keeps your portfolio in alignment with your long term goals.

Reviewing your portfolio for potential rebalancing at regular intervals and after significant market moves is one way to be sure that your advisor is helping you stick to the plan.

WHAT ARE THE POTENTIAL DRAWBACKS OF REBALANCING?

Selling High And Buying Low

Selling the best performing asset classes in favor of the lower performers seems counterintuitive. By doing so, you may be sacrificing potential long term returns. This should come as no surprise because stocks have historically produced higher returns than bonds over long periods.

The key here is that as your expected rate of return increases over time, so does your portfolio’s risk. If your allocation no longer aligns with your risk tolerance, you could be in for a rude awakening when (not if) the market experiences its next rough patch.

Corrections are an inevitable part of being a long-term investor. Thinking that this time is different always ends badly.

Transaction Fees and Taxes

As trades are entered to rebalance your portfolio, there may be transaction fees and/or commissions involved.

If you work with an advisor whose compensation is derived all or in part from the commission paid to them, this type of situation should raise some questions in your mind.

While sometimes it is impossible to avoid transaction fees, there are many cases where these costs can be avoided altogether. This is why it is critical to work with a fee-only CERTIFIED FINANCIAL PLANNER whose fiduciary duty requires them to avoid unnecessary fees.

Furthermore, rebalancing can trigger capital gains, which may be taxable. Your advisor should be cognizant of your tax situation, but sometimes this is unavoidable. It is usually better to pay some extra taxes on investment gains than to experience significant losses during the next market correction.

FINAL THOUGHTS

Successful investment management starts with having a strategy and sticking to it.

Periodic rebalancing ensures your investments do not stray too far from your strategy

If you’ve hired a fee-only CERTIFIED FINANCIAL PLANNER who acts in a fiduciary role, it is their job to do everything they can to help ensure your financial success.